SEC Fair Funds: Strategies for Solving 3 Key Recovery Challenges

SEC Fair Funds resemble standard securities class actions settlements, but their goals and the parties involved differ. Most notably for investors, Fair Funds have specialized requirements that can make participation more difficult.

As a regulatory agency, the U.S. Securities and Exchange Commission is chiefly focused on regulation and deterrence – not investor compensation. To participate in Fair Funds, investors must “play by the rules” and conform to the SEC’s standards and processes.

If these hurdles are cleared, however, Fair Fund recovery opportunities can be significant. In 2024, the SEC has already established nine new funds worth $474 million, putting this year’s activity well above last year’s total of $236 million (spread across seven funds).

The difference between a successful recovery and a rejection frequently boils down to the small details. With that in mind, let’s examine the most common recovery challenges FRT sees with Fair Funds and our team’s best practices for navigating them.

Challenge #1: Documentation Requirements

The strongest barrier to investor participation in Fair Funds is the SEC’s requirement for third-party trade substantiation records. The agency ideally wants to see 100% documentation for every holding and trade, proven by custodial and brokerage records created at the time of the activity.

These requirements make Fair Fund participation especially difficult for older claim periods, when records are difficult to retrieve or no longer exist because the time required for preservation has passed. A recent example is the upcoming $152 million Fair Fund involving Weatherford International, which has a claim period spanning 2009 to 2012.

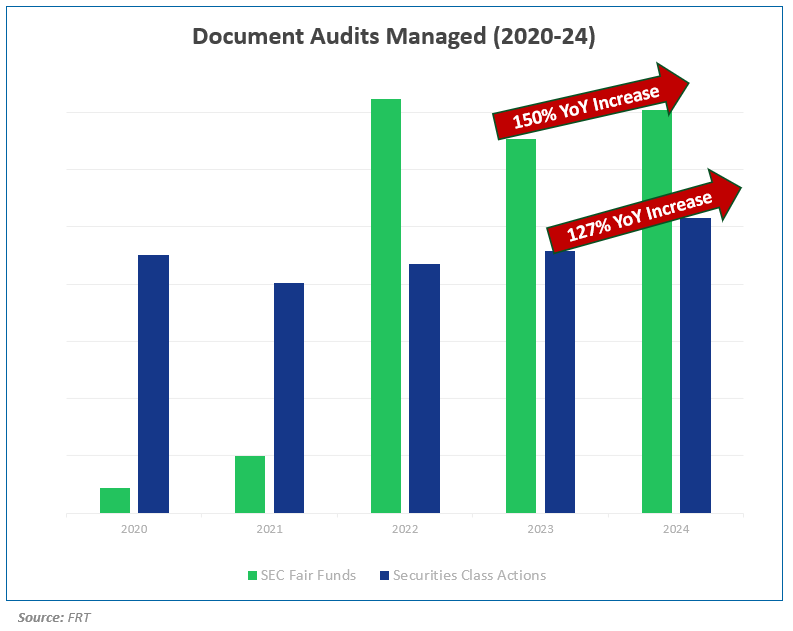

Claim administrators also have not taken a uniform approach to these requirements. More recently, however, we’ve seen more audit requests from the SEC and more strict enforcement by administrators. As on our recent FRT Market Insider session, Fair Fund-related audits for clients have risen significantly in 2024 – and we expect that trend to continue.

Our Approach: Alternative Documentation

When permitted, FRT has used affidavits from clients testifying to the reliability of system records either from third-party sources (e.g., custodians and prime brokers) or even the reliability of a client’s own systems. This approach is often necessary when third-party records have not been preserved over time or are otherwise difficult to obtain.

Challenge #2: Faster Administration

Compared to securities class actions, Fair Fund administrations have tighter turnaround times and more rigorous compliance demands. For example, deadlines for responding to SEC document requests are more strictly enforced, and investors have less room for error when the documents do not exactly match data submitted on the claim form.

And while it’s not uncommon for courts to permit exceptions that expand participation in class action settlements – such as accepting claims filed late if distributions have not yet occurred – the SEC does not give investors an opportunity to “save” their claims by substantiating other holdings and trades. Instead, all claims are effectively rejected.

Our Approach: Proactive Communication

As a best practice, FRT routinely works with claim administrators to understand the types of records accepted for a Fair Fund submission to maximize our clients’ lead times for document retrieval. In some cases, this also allows firm to better assess whether the time required to gather the required records outweighs the potential recovery opportunity.

Persistent and proactive communication with Fair Fund administrators has enabled FRT to streamline document retrieval and optimize claim submission for clients.

Challenge #3: Remittance

The SEC requires that 100% of Fair Fund payouts be distributed to the beneficial owners, without subtracting any contingent fees. This creates an operational hurdle for investors that work with a third-party filer and normally elect to pay a contingent fee out of the total pool of funds recovered from a given settlement.

As a result, some third-party filers have either started requiring upfront payment from clients or stopped servicing Fair Funds altogether.

Our Approach: Adaptive Processes

FRT has adapted its internal workflows to minimize any disruptions the SEC’s evolving requirements have on our clients. This includes establishing remittance processes that comply with SEC requirements – in ways that can be audited if needed – while still allowing our team to service clients within their existing agreements.

The Key Difference-Maker? Support

In the U.S., many securities class action settlements are routine – to the point that FRT can automate much of the recovery process for our clients. But Fair Funds have become a major exception. We have increasingly seen faster distributions with stricter requirements that tend to exclude more claims than they include.

That’s why post-claim submission support has become a critical area where third-party filers can deliver value. FRT is no stranger to challenging administrative decisions when we feel the penalties for document audit failures are too broad, because we understand that harmed investors aren’t paid out unless they survive “the full gauntlet.”

FRT will never sell, share, or rent your email.