No Claim Form, No Problem: Managing Atypical Class Action Distributions

When investors are harmed by securities fraud, they normally receive a class action settlement notice that provides case details and instructions for submitting a claim. But what happens when a case has no claim form?

No Claim Form (NCF) cases are securities class action settlements in which eligible investors receive compensation automatically, without needing to file a claim. These disputes typically arise from corporate mergers, go-private deals, and similar transactions, where eligibility can be determined from corporate or third-party records. As a result, payments are sent directly to eligible shareholders based on these records.

While this approach is more efficient than typical class actions, NCF cases inherently bypass the traditional notification process, with proceeds distributed to the shareholders of record. Custodians must then identify and credit the accounts of their beneficial owner clients, leaving nominees to navigate a complex allocation process.

As a result, NCF procedures can create substantial operational challenges around:

- Notification. Beneficial owners may lack visibility into whether NCF cases have settled, when to expect payments, or which parties will transmit the settlement funds.

- Verification. With limited advance notice, both beneficial owners and nominees may have difficulty tracking down eligible securities within their data. They also cannot easily ensure the distributing party (e.g., a claims administrator) has correct contact information, as case eligibility is based on shareholders of record registered by the DTCC or on the issuer’s ledger. Furthermore, years have often passed since the challenged transaction has occurred, meaning beneficial owners, or even nominees, may have moved or closed.

- Allocation. Particularly for investment management and wealth firms, determining how to allocate payments across their underlying client accounts is an additional burden. Identifying and locating eligible shares that were on loan or shorted during the class period presents further complexity, as the short seller, borrower, or third-party purchaser may have appeared to be the beneficial owner at the time.

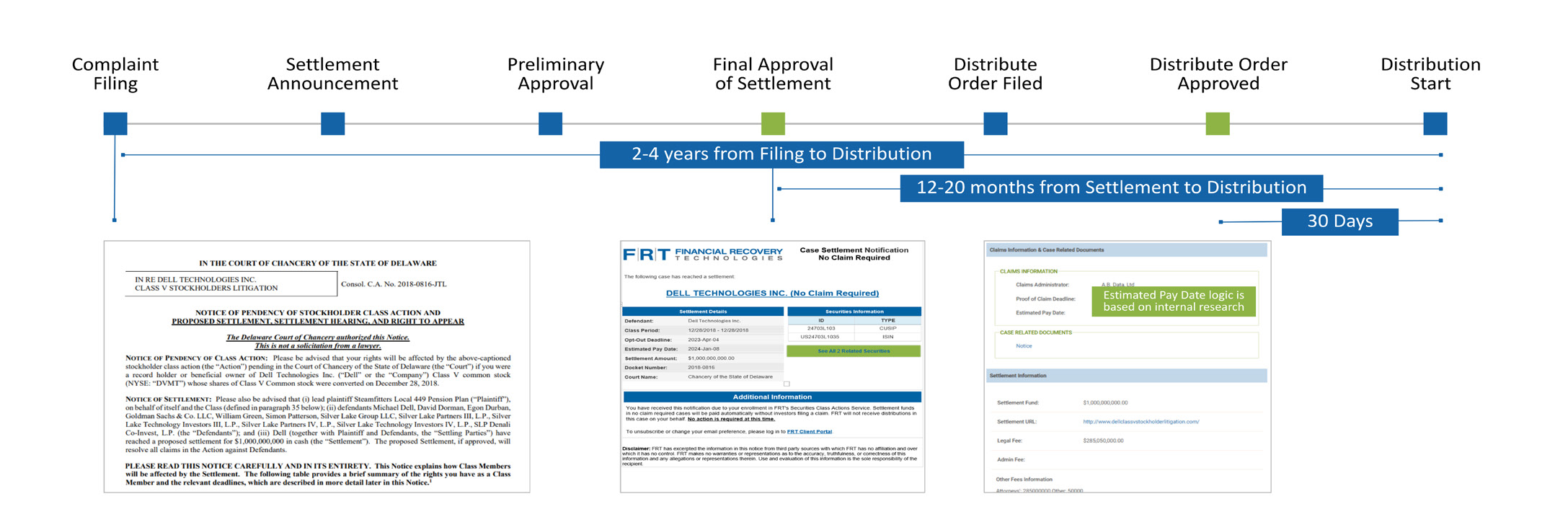

Amplifying these challenges are NCF cases that have settled for large amounts. Several settlements have exceeded $100 million in recent years, such as the $1 billion class action involving Dell Technologies. With large distributions especially, the deposited funds can create a fire drill for internal operations teams if they are not diligently monitoring these cases.

With material client recoveries at stake, we suggest the following strategies for maintaining visibility into NCF cases and managing the allocation process more effectively.

Knowing Where to Look

In most years, FRT sees roughly 20 to 30 No Claim Form cases settle in various North American courts. We can bucket most recovery opportunities into a few groups:

Delaware Breach of Fiduciary Duty: Many NCF cases originate in the Delaware Court of Chancery and involve mergers. These disputes, like the Dell example, lend themselves to a no-claim process because eligibility is simply determined by individual holdings on the transaction’s effective date. The class period is often just a single day. Payouts can be significant given that many large public companies are incorporated in Delaware.

Special Purpose Acquisition Companies: In these disputes, plaintiffs may allege that the acquisition target was worth less than the value represented by the defendant SPAC (i.e., less than par value). Investors who did not exercise redemption rights can be identified from corporate records and can receive a base amount of compensation* without the use of claim forms.

*To determine the full extent of the damage suffered by shareholders, investors must submit a claim form detailing when they sold their shares on secondary markets. This wrinkle makes SPAC cases “hybrid” recoveries, with NCF and traditional elements.

SEC Fair Funds: The SEC recently began requiring that Fair Funds be remitted directly from the administrator to the underlying account holders, without passing through another party. Most Fair Funds do still require claim filing. Where shareholder eligibility is more easily defined or a previous class action allows them to identify claimants, however, the SEC has sometimes forgone the typical claims submission process.

For example, in the United Development Fair Fund, investors whose eligibility could be determined from a related securities class action (In re United Development Funding IV Securities Litigation) and defendant records received a distribution payment with no further action required.

Canadian Class Actions: In some cases, Canadian courts have required that payments go directly to eligible shareholders.

How Investors Can Respond

Beyond knowing where to look, investors can especially benefit from understanding what case-level data will help their teams appropriately plan for upcoming distributions.

With no claim forms to file, class action specialists like FRT are not directly involved in NCF recoveries. However, investors outsourcing class actions to a third party can (and should) use their providers to monitor and provide guidance around upcoming NCF payments. For example, FRT’s U.S. Settled solution keeps clients updated on the status and details of No Claim Form recoveries – with timely alerts that give client operations teams the parameters they need to streamline allocations.

For investors that self-service these cases today, the following data points can help you better navigate NCF distributions.

Case Timeline Outputs:

- Settlement and distribution timing

- Estimated payment date

- Payment source

Advance settlement notification allows investors to track case progress and plan for future recoveries. Knowing when a distribution order is court-approved signals that payment will begin soon, giving investors valuable lead time for allocation work. Lastly, identifying whether the NCF payment will come from the DTCC or a claims administrator allows investors to prepare their systems to accept the incoming funds and, if necessary, reach out to verify that payment and address information are up to date.

Client Allocation Inputs:

- Class period

- Eligible securities

- Pro rata amount

- Shares outstanding

Several inputs are needed to manage NCF allocations properly. Collectively, this data enables investors to estimate how much money they’re receiving, validate whether they are missing recovery dollars, and then allocate payments received into which accounts held eligible securities on the relevant date(s).

Conclusion

Large class action settlements can magnify several aspects of the recovery process – allocation complications, fiduciary risk, and urgency, to name a few. Having regular visibility into NCF case data, ideally consolidated on a platform with the rest of your firm’s class action recovery data, addresses much of this operational friction proactively. Ultimately, it helps ensure that clients receive their full entitlements to the correct accounts.