Chinese Companies Increasingly Held Accountable in U.S. Class Actions

Class actions in the United States are a consistent and reliable means of enforcing shareholder rights. U.S. law provides strong legal protections for shareholders and a passive system through which claimants can take part in settlements with no legal or financial risk. On average, we have seen around 200 cases settle each year, representing approximately $5 billion in annual recoveries.

Conversely, China features a nascent class action system with only one successful case documented to date and numerous obstacles for shareholders. As one of the world’s five largest economies by GDP, however, Chinese markets remain widely attractive to investors in Asia and elsewhere.

As a result, the U.S. legal system provides the only realistic means to hold Chinese companies accountable for securities fraud and provide investors with legal recourse via class actions. Recent U.S. settlements involving China-based companies also highlight significant recovery opportunities for investors with exposure in these cases.

For more on the global shareholder recovery landscape, download FRT’s 2025 Securities Class Action Intelligence Report.

Understanding American Depositary Receipts and Nexus

As of June 2025, there are approximately 280 Chinese companies trading in the U.S. via American Depositary Receipts (“ADRs”). ADRs are a type of security issued by banks that allow U.S. investors to gain exposure to stocks traded on foreign markets without trading directly on foreign exchanges. ADRs may be listed on U.S. exchanges in U.S. dollars and can be traded, settled, and held as if they were ordinary shares of U.S.-based companies. The underlying shares are generally purchased by a U.S. bank from a foreign exchange and are held in an overseas branch.

Many of the largest and most familiar foreign companies, including those in China, trade in the U.S. through ADRs, and they make up an active part of our securities markets. In fact, we saw two high profile shareholder class action settlements involving China-domiciled companies listed on U.S. exchanges in 2024. Alibaba settled for $433.5 million and was one of the year’s largest recoveries, while Luckin Coffee resolved for $175 million. These settlements are the result of a significant increase in the number of Chinese ADR cases filed during the past several years.

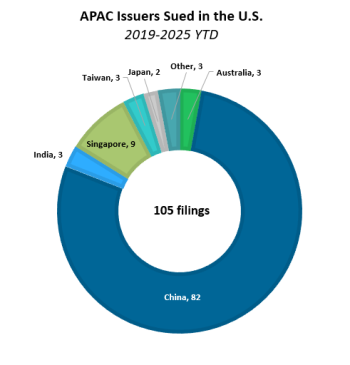

In recent years, roughly 20% of all shareholder class actions filed in the United States have been on behalf of investors who purchased ADRs in foreign companies and later suffered losses as a result of those companies’ behavior. The chart on the right illustrates the number of APAC companies that have been sued in U.S. class actions in recent years.

There were 105 actions against APAC-domiciled companies from 2019 through May 1, 2025, the vast majority of which were against Chinese companies. That’s 82 out of 280 Chinese companies that have been sued in U.S. class actions, or nearly 30% of all Chinese companies trading through ADRs on U.S. exchanges.

For a U.S. court to have jurisdiction over a securities class action involving ADRs, there needs to be a nexus, or link, between the claims being brought and the United States. Investors based outside of the U.S. can join these actions as long as they purchased the ADRs on U.S. exchanges. That provides sufficient nexus for recovery in these actions.

We expect this trend to continue and to see the number of class actions against Chinese companies increase in future years, given that China’s class action system does not currently provide a viable path to recovery for most shareholders.

Chinese Class Actions Explained

China has a class action system that permits two types of representative shareholder suits: an opt-out system initiated by two government agencies and an opt-in system initiated by shareholders.

The opt-out system allows for class actions against companies on behalf of all eligible shareholders on record who held the company’s shares during a relevant time. However, it has only been successfully used once. In 2021, the class action against Kangmei settled for $385 million. Despite Chinese regulatory agencies pursuing over 35 investigations into Chinese companies, we have not seen any additional class actions filed since.

The Chinese government controls when and if such suits are filed. Prior to 2021, China rewrote its class actions laws, and Kangmei was an opportunity for China to show that it had a system in place to punish fraudulent companies and provide investor recoveries, and to make an example of one such company. But the government has not shown any interest in pursuing additional cases.

China also has an opt-in system by which investors can initiate class actions proceedings. But it has several key impediments that make it very difficult to bring such private cases. Chinese law does not permit contingency fees, and there is no existing market for litigation funding in China; so, to bring such actions, investors need to self-finance and pay ongoing legal fees, which is prohibitively expensive.

Further, Chinese courts have thus far limited class actions to a narrow segment of cases involving limited types of disclosure violations. They have also required that judges find sufficient evidence for cases to proceed, which in practice means there must have already been administrative punishments, criminal judgments, or admissions of guilt by a defendant company relating to the fraud. Typically, those do not exist. Given these challenges, we do not expect to see any class actions filed via this opt-in system.

Without viable options in China and with continued instances of fraud, we expect the trend of significant recoveries here to continue.

A Word of Caution: Geopolitics

The U.S. presidential administration has threatened on several occasions to delist Chinese companies from U.S. exchanges. Most notably, U.S. Secretary of Treasury Scott Bessent said in March that this option remains on the table and will ultimately be the President’s decision.[1] Congress has also been saber-rattling about the same, with a group of ten congressmen from both parties sending a letter to the Securities and Exchange Commission in May calling for the delisting of Chinese companies with strong ties to the Chinese government.[2]

Given the number of Chinese companies trading on U.S. exchanges, and the billions in capital involved, it seems unlikely that either the administration or Congress will wholesale delist Chinese companies, which would cause havoc in the market. More likely, the administration will target certain Chinese companies and force them to delist.

There is precedent for such actions. During the first Trump administration, the President issued an executive order delisting three Chinese telecommunications companies from U.S. exchanges that were identified as having ties to the Chinese military. Further, in 2022, the U.S. Government sought to impose greater financial disclosure requirements on Chinese companies. Rather than comply, several voluntarily delisted and either relisted on the Hong Kong Exchange or went private. There would likely be a similar response here if some Chinese companies were forced off U.S. exchanges.

While the fate of certain Chinese companies trading on U.S. exchanges may remain uncertain, the pace of U.S. class actions against them overall is not expected to diminish. For now, Chinese companies will continue trading on U.S. exchanges via ADRs, with many settling and providing significant recovery opportunities for investors.

Class Action Market Research

FRT’s 2025 Securities Class Action Intelligence Report analyzes hundreds of shareholder class action filings, settlements, and payouts from 2020-24, both in the U.S. and internationally. Download our proprietary briefing for timely market insights that we hope investors can use to make more informed filing decisions.

[1] Economic Times, Delist Chinese Stocks from US Indices? Trump Administration Says Everything’s on the Table (Apr. 8, 2025)

[2] Van Bramer, James, Lawmakers Ask SEC to Delist Chinese Stocks From US Exchanges, Plansponsor (May 12, 2025).