Case Spotlight: DiDi Global ADS Settlement ($740 Million)

A United States federal court recently approved a $740 million settlement resolving shareholder claims against China-based rideshare app developer DiDi Global.

With the approval, In re DiDi Global Inc. Securities Litigation becomes one of the 10 largest U.S. securities class actions of the past decade. The settlement deserves attention not only for its size, but also for the underlying allegations and their implications for global investors.

Continue reading for analysis of the DiDi resolution and factors worth considering as the claim filing process begins.

Background

- Claim deadline: April 6, 2026

- Class period: June 30, 2021 – July 21, 2021

- Settlement size: $740 million

Plaintiffs allege that DiDi misled investors during its 2021 initial public offering by failing to disclose that Chinese regulators had raised serious concerns about the company’s data security practices. Nevertheless, DiDi forged ahead with its IPO, raising $4.4 billion through American Depositary Shares (ADS) traded on the New York Stock Exchange.

Shortly after the IPO, Chinese authorities launched a cybersecurity review of DiDi, removing its apps from domestic platforms and halting new user signups. These events preceded a sharp decline in Didi’s share price and ultimately led to its delisting from the NYSE in 2022.

A Rare, Significant Recovery Opportunity

DiDi is the largest U.S. securities class action announced since 2023, when two shareholder suits against Dell and Wells Fargo each resolved for $1 billion. In most years, only one or two settlements exceed $500 million.

With just a 22-day class period, the DiDi eligibility pool is also more concentrated than typical large securities cases. Public records indicate that large institutional investors had relatively limited exposure to the IPO – a dynamic that could result in more favorable pro rata payouts for smaller and mid-sized DiDi shareholders.

The U.S. Remains a Critical Investor Recovery Avenue

Despite shifting public discourse around shareholder rights in the U.S., where some have criticized the class action system, the DiDi settlement reinforces the critical role of American securities law for both foreign and domestic investors. Why?

First and foremost, DiDi has not returned to U.S. trading markets since delisting four years ago – making this case the only realistic path to recovery for aggrieved investors. Further, the U.S. is particularly important for investors with exposure to markets where group shareholder recovery is restricted or unavailable, such as China. Without U.S. shareholder protections, such investors would have been denied access to justice and compensation for their losses.

The U.S. class action system stands apart for the quality of protections afforded shareholders and its efficiency. From 2023-25, investors recovered more than $17 billion from securities class actions, with many of these cases settling less than three years after the initial filing.

The early weeks of 2026 suggest this year could be especially robust, with DiDi and three other nine-figure settlements driving more than $1.4 billion in net-new recoveries.

Oversight & Regulatory Implications

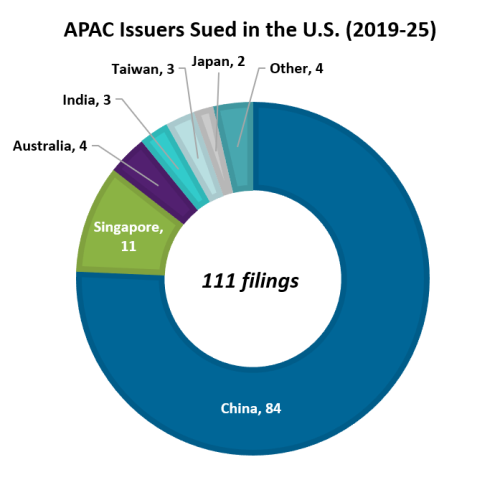

DiDi continues a pattern of large recoveries involving China-based issuers trading on U.S. exchanges via ADS instruments. Recent examples include the $433.5 million Alibaba class action and the $175 million Luckin Coffee settlement. These outcomes follow a wave of suits filed against China-based issuers in recent years, as the chart to the right shows.

What makes the DiDi settlement so striking is its size relative to other high-profile IPO disputes, such as the $200 million case involving Uber. Despite lacking a large institutional lead plaintiff, DiDi class counsel delivered an outsized win for shareholders – highlighting both the seriousness of the alleged misconduct and the potential role of geopolitics.

Since 2019, more than 80 Chinese companies have delisted from U.S. exchanges, as regulators have raised their scrutiny of foreign issuers seeking access to American capital. The trend of Chinese company departures will likely continue given the economic and political tensions between the two countries. Eventually, SEC enforcement proceedings against DiDi could yield a Fair Fund on top of this class action.

Key Filing Considerations

As with other large U.S. settlements, investor recovery outcomes in the DiDi case will rest heavily on the deficiency process – in which administrators vet all claims filed by investors.

In response to a recent surge in fraudulent filings, these administrators are applying increasingly rigorous scrutiny to claim submissions. Even small discrepancies, such as missing transaction data or substantiation records, can result in partial or full claim rejection. High-value claims are likely to be audited.

With a claim deadline of April 6, 2026, investors are encouraged to begin gathering relevant documentation now to ensure submitted data is complete, accurate, and defensible.

Looking Ahead

The DiDi settlement represents a rare convergence of scale, timing, and global relevance. To learn more about how our Legal and Operations teams are handling this case for FRT clients, contact us via the form below.