Brambles Judgment Reinforces Australia as a Favorable Recovery Venue

Earlier this month, the Federal Court of Australia ruled in favor of class members in Southernwood v Brambles Limited [1] – a significant decision for investors as the country’s first class action to succeed following trial.

For years, Australia has generally been a favorable jurisdiction for securities litigation. However, most meritorious cases settle before the court issues a judgment. In Brambles, following trial, a federal court ruled in favor of investors both on the defendant company’s liability and on causation and damages. The decision helps to clarify key issues of Australian law and will inform future cases.

Read on for analysis of the Brambles judgment and what it means for shareholder recovery efforts in Australia.

Unpacking Brambles

In 2017, Brambles (BXB) publicly downgraded its estimated sales and profit growth, after which the company’s share price declined significantly. Shareholders brought a class action against the company, alleging its management knew about the underlying business challenges and failed to correct its projections in a timely manner. The plaintiffs claimed that Brambles made misleading statements to the market and breached its continuous disclosure obligations regarding its sales and profit guidance.

With the Federal Court ruling in favor of the class, the decision carries two implications for future investor claims in Australia.

First, the outcome reinforces that class members can recover against companies when they issue misleading forecasts and guidance, including violations of continuous disclosure obligations – i.e., their ongoing duty to disclose information that materially influences firm performance or share price.

Second, the court applied a market-based per share inflation model in calculating shareholder losses. This type of model benefits investors by assuming that the market is efficient, and that affected individuals purchased shares at the same inflated price. In turn, it removes the need for plaintiffs to prove that each purchase relied on the company’s alleged misstatements, making it easier to establish losses using market data.

Ultimately, the decision could serve as a roadmap for what claims are alleged and how losses are proven in future cases.

Potential Implications for the CBA Ruling

Brambles is especially notable in the context of an earlier securities class action against Commonwealth Bank of Australia [2] (“CBA”), during which the court ruled against claimants on loss causation and damages.

In 2024, the presiding judge wrote that CBA management’s prior knowledge of systemic non-compliance, and the associated financial risks, would be unlikely to “influence persons who commonly invest in securities in deciding whether to acquire or dispose of CBA shares,” had that information been disclosed in a timely fashion.

The CBA judgment is now under appeal before the High Court, which as Australia’s top judiciary exerts authority over any single federal court ruling, such as Brambles. While the CBA case involves broader questions of law, the High Court could be persuaded by the Brambles decision when it comes to continuous disclosure obligations or the market-based inflation issue. Alternatively, the High Court could sidestep these specific issues entirely in the CBA appeal, instead focusing on other elements of the case. Brambles defendants may also appeal this latest judgment.

How these cases ultimately resolve could embolden corporate defendants to take more shareholder disputes to trial, or they could broaden the tactics available to the plaintiffs bar. The Brambles decision suggests the latter, but we await further rulings. In either scenario, Australia’s legal framework for investor recovery is active and evolving.

Australia’s Shareholder Recovery Outlook

Like the United States, Australia has an “opt-out” class action framework that includes harmed investors in the wider class by default. Eligible investors can either participate by registering a claim passively – removing financial or reputational risk – or else exclude themselves from the class and pursue direct legal action.

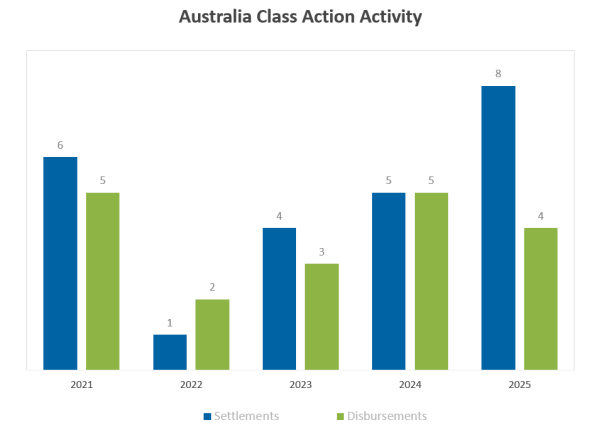

As a result, Australia’s class action system has made it one of the more accessible jurisdictions for shareholder recovery. Recent activity bears that out: eight cases settled in 2025, including BHP Billiton ($110 million), Crown Resorts ($72.5 million), and Treasury Wine Estates ($65 million), while another four disbursed to the class.

Australia should remain a strong jurisdiction for shareholder recovery in 2026. Recent cases have returned close to 38% of investor losses on average – a higher mark than comparable outcomes in the U.S. Earlier this month, a2 Milk agreed to settle a pending class action for $62 million, with additional settlements and disbursements expected later in the year.

For funds with exposure to Australian equities, the question is less whether class actions deserve their attention, and more whether their current class action process is built to take advantage of Australia’s class actions system and reliably capture eligible recoveries.

To learn more about global shareholder litigation or how FRT approaches claim filing in other jurisdictions, download the 2026 Class Action Intelligence Report for proprietary research and insights.

[1] Southernwood v Brambles Limited (No 3) [2026] FCA 418

[2] Zonia Holdings Pty Ltd v Commonwealth Bank of Australia Limited (No 5), [2024] FCA 477 (May 10, 2024)